Real Estate Market Insights: Data & My Thoughts

Real Estate Market Insights: Data & My ThoughtsBelow is an excerpt from last week’s Invested Equity Passive Investor newsletter, where I shared some economic data and a few thoughts on the market.

Economy

The Fed remains committed to taming inflation down to 2%.

They likely took it as a positive sign when the Core PCE 12-month average for December came in at 2.9%.

However, it was not enough for the Fed to promise rate cuts by March.

The labor market remained robust throughout 2023, but January’s numbers came back below expectations.

It’s unclear whether this marks the start of a downturn in the labor market or merely a short-term pullback.

Meanwhile, consumer confidence hit a two-year high after increasing for three consecutive months.

Home Sales

Mortgage rates came off two-decade highs in October 2023, settling at around 6.6% by the end of December.

While still over double the low rates of 2021, pending single-family home sales increased by 8.3% nationally from November to December.

Broken down by region, the South enjoyed an 11.9% increase in pending home sales, while the West experienced a significant 14% jump.

Existing home sales declined by 6.2% YOY in December, but the median sales price increased by 4.4% YOY.

Housing Inventory

Inventory increased from 2.9 months in December 2022 to 3.2 months in 2023, based on the current pace of sales.

New residential housing (single-family and multifamily) permits decreased by 11.7% in 2023 from 2022, and housing starts decreased by 9% in the same period.

This chart illustrates the total number of new residential housing permits and starts.

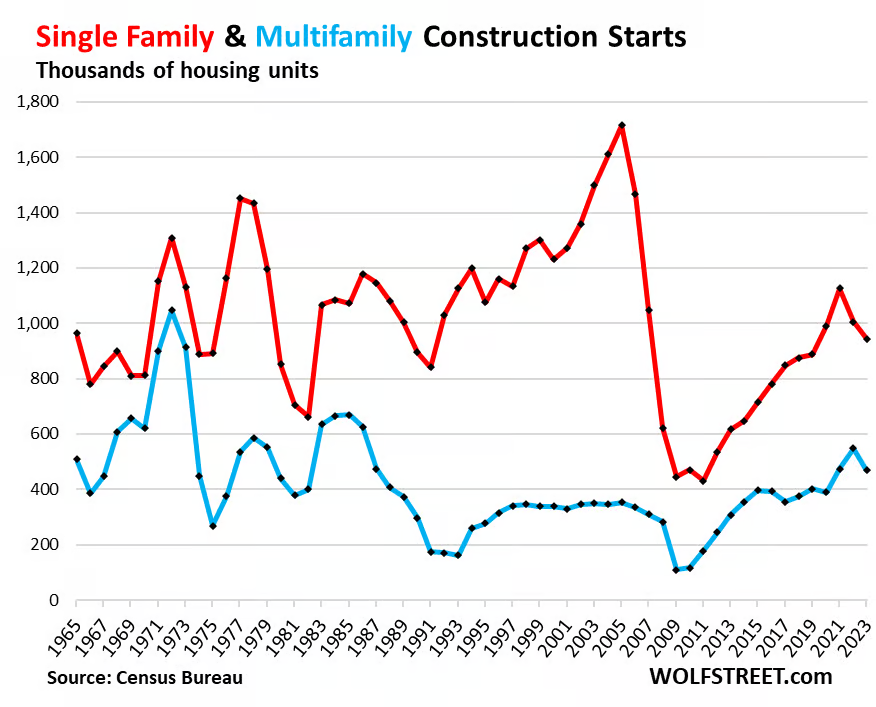

This chart breaks down single-family and multifamily starts:

Rent Growth

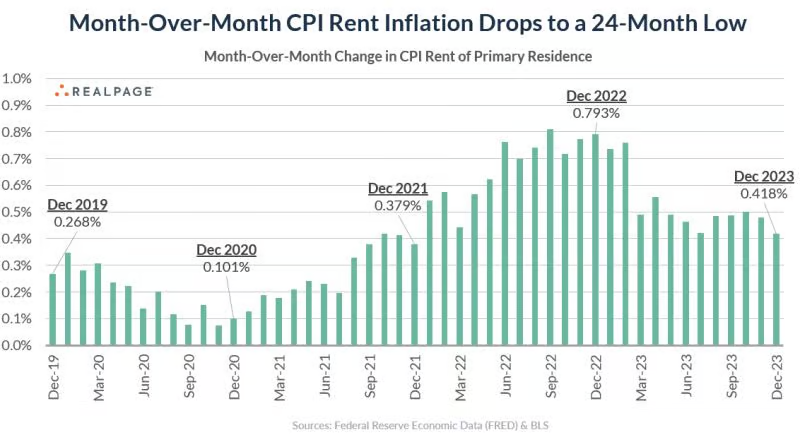

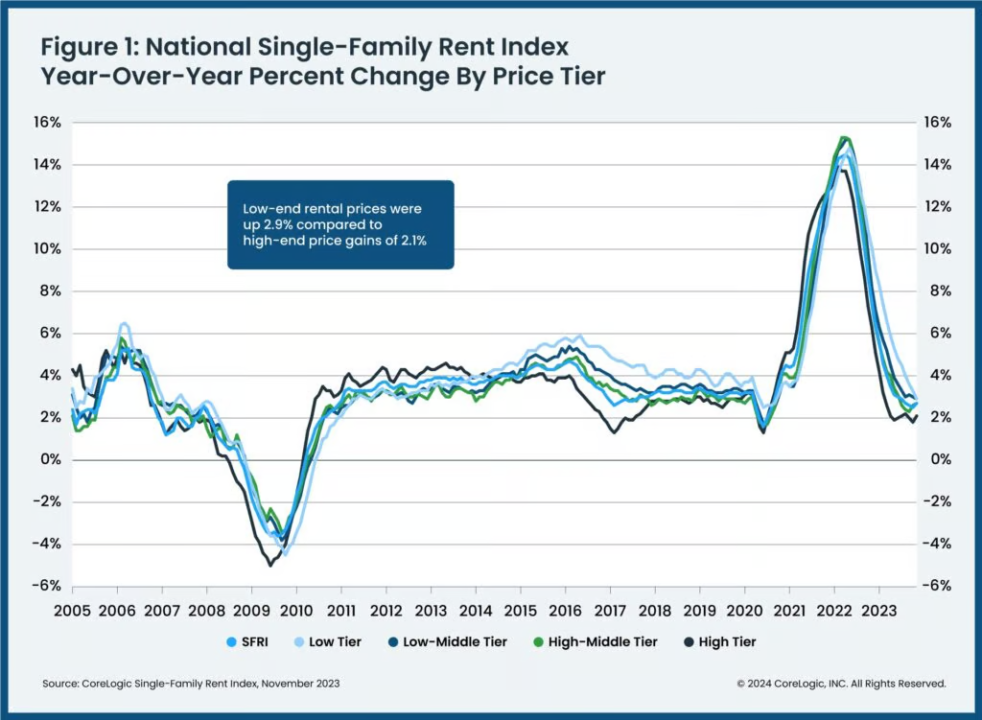

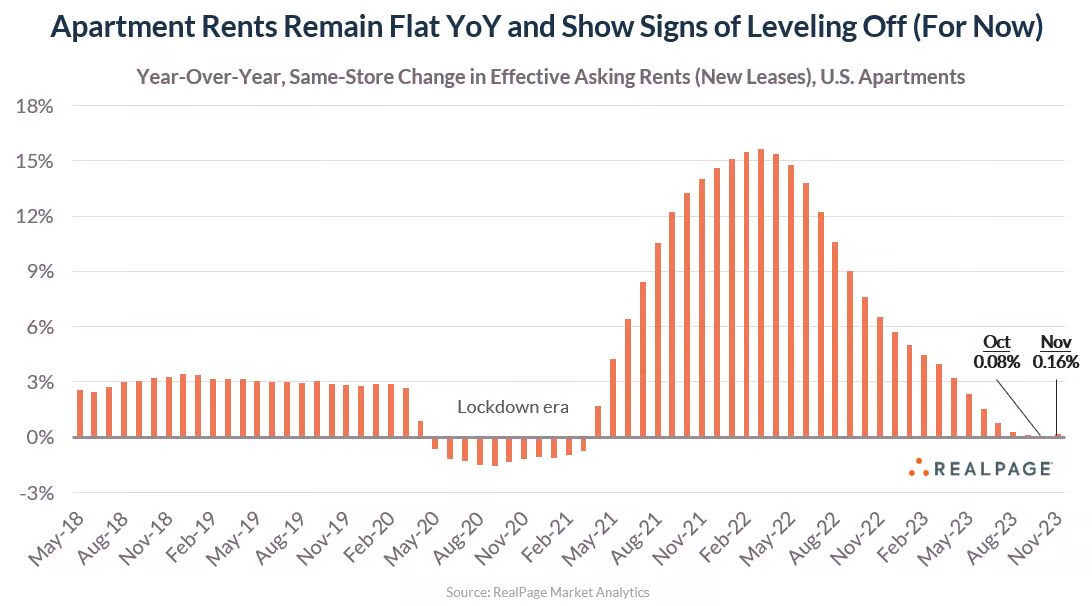

Rent growth sharply declined from its 2022 highs, as expected.

According to CoreLogic, single-family rent growth in November 2023 came in at 2.7% YOY.

Multifamily rent growth barely remained in positive territory in November, increasing only 0.16% YOY.

Summary

The residential housing market isn’t without challenges, but it remains healthy overall.

Homeowners are stilling on a record high of $32.6 trillion in equity.

There is enough demand for the current (low) level of available inventory to keep home sales price growth steady.

With new housing construction permits and starts declining, additional inventory must come from existing homeowners.

Considering that over 82% of mortgaged homeowners have a rate below 5%, many are hesitant to sell while interest rates remain above 6%.

Rent growth in 2024 will likely remain in the 1-3% range nationally.

Multifamily operators in markets that have had a significant number of new units hit the market will continue to face near-term headwinds filling vacancies.

With the pullback in new construction permits and starts though, multifamily operators should enjoy stronger rent growth for a year or two once the stockpile of completed units are absorbed.

Caveat

It’s important to consider both macro and microeconomic factors when evaluating investment opportunities.

An experienced operating team, the right asset, and a strategic location in the market are all crucial elements for achieving long-term projections.